Tax season is over. Take a deep breath – whether you’re a bookkeeper or tax preparer, you’ve endured plenty of stress these past months, and now you’re in the perfect space between vacation and conference season to look back and figure out how to make it go better next year.

That’s what we do in our firm, anyway; I learned an amazing lesson from one of my favorite instructors, Tom Gorczynski, to plan for next tax season while the pain is still fresh in your mind! We schedule a company-wide zoom meeting, and everyone fills out a survey beforehand that asks about what worked, what didn’t, what they’d like to see go differently, who their favorite and least-favorite clients are, and why. This helps us incrementally improve year-over-year, and makes sure everyone has a voice. Then we send out cocktail kits and snacks to everyone, we celebrate, and we brainstorm. We even vote clients “off the island” together.

One of the themes that comes up every year is the need to move more clients off QuickBooks Desktop and onto QuickBooks Online. I know, groan… yet another talking head telling you to make the shift! At this point you’ve been bombarded with information on all the benefits of moving to QBO, so I won’t bore you with those. I’ll just share my own experience.

It was becoming more and more of a drag to coordinate with Desktop clients to review their books, and the new subscription structure made it confusing and frustrating to know who was on which version and how to make the most of what they were paying for. And of course, there were constant client fears around Intuit’s messaging, worrying they were going to stop supporting their product. But the biggest stressor for us was that it was actually getting hard to find junior bookkeepers who had ever worked with the Desktop program. (No joke. How about that for making a certain dancing accountant feel old?)

I assure you, I absolutely *hated* QBO for years; it was a clunky beast that didn’t have some of the most basic functionality that Desktop did – and I’m not just talking about the early days; this went on far too long and alienated many users. And while I held out for ages in moving to QBO, especially for certain types of clients that really benefited from what QBDT had to offer, I finally realized that it’s gotten to the point where the features I love about the Online version far outweigh its negatives. Between the concerted effort that Ted Callahan, Jessica McCracken and their team have made to actually listen to our community and implement some of the most-loved features; the fact that most third-party apps and tools no longer work with Desktop; and the advent of RightTool, an amazing browser extension by industry superstar Hector Garcia that supercharges what QBO has to offer… it’s time. It’s really time. QBO is now light-years ahead of almost anything that QBDT can do.

The point of outlining all this isn’t to convince you that you should migrate your remaining Desktop clients to QBO. It’s to suggest that when you do – follow my lead, and use exactly these reasons in your messaging. This became our mantra for communicating the value of converting, and it worked; at this point we only have one client left who needs to make the shift.

Think about it: your clients and your team members trust you, more than anyone else, to make smart and thoughtful decisions with everyone’s well-being in mind. If you convey the messaging that QBO is listening to us and responding to our requests, that RightTool will make you more efficient, and third-party apps will serve your clients’ needs better than the previous solutions, they will believe you, you’ll get buy-in, and in our experience, we found that clients were overwhelmingly positive and enthusiastic (though understandably still nervous) about the change.

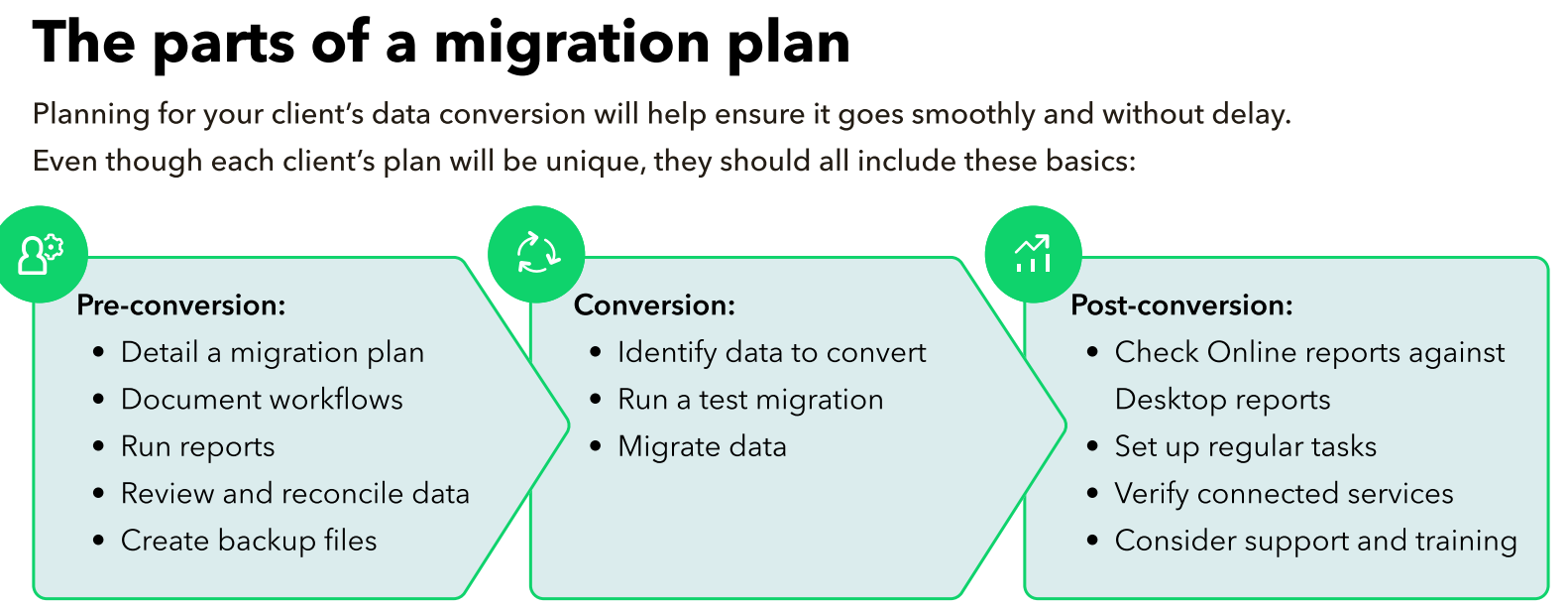

Once you’ve got buy-in, it’s a simple matter of following some practical tips and advice to make sure the execution is done well.

- Understand the Conversion Process

Intuit came out with a free conversion tool a few years ago that they keep tweaking to make it better; the most recent improvements announced at last year’s QB Connect blew me away – you can now batch migrate clients, meaning “do a ton at once and be done with it”. To be honest, it kind of made me wish I had waited to convert some of ours! However, as straightforward as they make it to migrate data from QBD to QBO, you do have to ensure your QBDT file is ready for the transition. This means backing up, running a verification on the file, ensuring it’s under the maximum target limit, and cleaning up any weirdo issues that have been hiding or buried for years, especially if you don’t regularly do a verification and rebuild. And most importantly, reviewing your “all dates” financial statements beforehand, exporting them, and comparing the same reports afterwards is essential. - Technical Resources for Conversion

I mentioned Intuit’s Conversion Tool, which guides you through the process step-by-step; they also have a QuickBooks Conversion Toolkit with checklists, webinar links, guides, client materials, and even a link to book a call to have Intuit do the conversion for you – just head here and then click on the “How to migrate” button to download the toolkit or set up a call. If you prefer your info from a third-party source, Hector Garcia does a short walkthrough on his YouTube channel, and Alicia Katz-Pollock is offering an Earmark webinar on May 21st. And if you have any concerns whatsoever about the process, consider outsourcing the job. We worked with CMB Hero and had a good experience, and I know DL & Associates does migrations as well; there are probably hundreds of companies or even trusted colleagues who’ve gone through the process before and can help you make sure it goes smoothly.

- Research Third-Party Apps Before Converting

There are some super-fabulous apps out there that we love to use for syncing daily Point of Sale data, such as Synder, Bookkeep, and Shogo. But you need to look at the client’s needs and determine how they’ll be met in the new QBO world before making the shift – not all sync programs work with all POS platforms. Do demos, consult with colleagues, and figure out the timeline for implementing – in other words, not only the migration of QBDT data to QBO, but setting up the new system to work with the POS and get it all running. Our experience has been that some up-front planning saves loads of effort on the far end (which is when you’re pressed for time so the client can get back up-and-running).

- Prepare Desktop Clients For The Change

And sticking with the theme of up-front planning… a little client hand-holding goes a long way. What they’re looking for is to follow your lead as their trusted advisor. The more you can compare and contrast their existing workflows and procedures with the new system, the more comfortable they’ll be with your proposal to move to QBO. Ideally, you already have Standard Operating Procedures in place for each of your clients. I wince as I type this, because I get that this is the “ideal” and not necessarily your reality – in all honesty, we’re still in the process of making sure each client has clear and detailed SOPs for every scenario. But this is a golden opportunity. Your instructions – in Word, an Excel checklist, Loom videos, or a project management app like Keeper, Financial Cents, or Asana – will build trust, making it much easier for you to illustrate to the client that this is a manageable change and that you’ve anticipated their needs. Side bonus: way less stress when a client (or your firm) loses a trusted team member and a new one needs to be trained ASAP.

To illustrate: in going through all the steps that a client’s office manager would complete each month as part of her billing process, and reproducing/ rewriting them using QBO, I noticed that she would no longer be able to run a particular report – at this point I had to decide whether we would come up with a different way for her to perform the same task, or whether we would track the data with a different feature in QBO so that she could run the report she was used to. Both approaches were fair; but the point is that I wouldn’t have noticed this change without walking through the process of retooling the procedures. This built trust with the client and made them more open-minded about making the change, because they knew we were actively anticipating and removing any stumbling blocks.

- Client & Staff Training and Familiarization

As you know, transitioning to QBO doesn’t just involve moving data; it’s also about adapting to a new user environment. You’ll want to invest time in training sessions provided by Intuit or certified trainers like Royalwise (my personal favorite – I’ve been studying from Alicia for as long as I can remember). Intuit also offers an ongoing monthly session called QBO In The Know, which I encourage all my team members to attend as part of their paid training hours – this ensures that you don’t just get up-to-date, but that you stay that way, as the QBO ecosystem is constantly improving and new features are released every month. Hector Garcia’s YouTube channel is an endless wealth of information (I once hired a senior accountant with no degree and no certification based on the fact that she learned QBO by watching every single one of his videos. She’s now our Senior Accountant). Lastly, remember that QBO has a demo company! It’s a sandbox – have at it, and let your team practice without the risk of affecting real data.

Start by getting your client and team members’ buy-in. Take advantage of the available resources, and invest in training. With communication and planning, both your firm’s and your clients’ bookkeeping experience will end up better than it was with Desktop – we don’t have a single client that regrets having migrated, despite the fact that we all miss this-or-that feature (everyone’s got their favorite). But I promise it will be replaced by a new favorite. Remember, the goal is not just to convert data, but to enhance the overall efficiency and effectiveness of your accounting practices and those of your clients.

So… take that deep breath, plan for the future, and enjoy the heck out of that moment next tax season when you hear someone go, “oh wow, this really is so much better than it used to be!”

Note! As my readers know, I am downright fanatical about transparency and full disclosure (often to my detriment, as you may have noticed that I have a wildly popular award-winning blog that is non-monetized). Though this particular post is a paid partnership with Intuit, I want you to know that a) I wanted to write an article on QBDT–>QBO conversions anyway, but couldn’t find the time; getting paid allowed me the break from client work I needed to make it happen; and b) they didn’t delete a single thing when I presented it. In fact, they were totally cool with all my Intuit-bashing… which made me pretty impressed with them, to be honest. That’s twice now — let’s see if they go for a three-fer!